Nancy J. Altman, cofounder of the group Social Security Works, debunks many of the pernicious myths about Social Security in the following Truthout interview:

Mark Karlin: Perhaps the most significant myth – because it creates a false underlying premise – about Social Security, fostered by those who oppose it, is that it is a government entitlement that is given to the elderly. However, we all earn Social Security, don’t we?

Nancy J. Altman: Absolutely. Social Security is wage insurance, which we earn through working and paying premiums or insurance contributions, under FICA, the Federal Insurance Contributions Act. Social Security insures workers and their families against the loss of wages in the event of permanent and serious disability or death, in addition to old age. These are events that can happen to any of us.

Most of us don’t like to think about our own vulnerability, but any of us can be hit by a truck or contract a life-threatening illness and wind up needing income to replace our wages for ourselves and our dependents. One out of three Social Security beneficiaries receives disability or survivor benefits, not retirement benefits. And I want to emphasize that Social Security’s benefits are earned. They are part of our compensation package, part of the pay we earn for our labor. The retirement annuities are deferred compensation.

Social Security’s life insurance is generally the most valuable employment-based life insurance workers have. And the long-term disability insurance is generally the only disability insurance Americans have. It is instructive to note that employers used to include Social Security in their descriptions of compensation. After all, they match, dollar for dollar, Social Security contributions made by their employees.

Of course, the most blaring myth about the government-administered pension program is that it is going bankrupt. Why is this so specious and false?

Social Security, in pension jargon, is current-funded. About 75 percent of its revenue comes from insurance contributions withheld from workers’ wages, matched dollar-for-dollar by their employers. This is a permanent and ongoing source of revenue. As long as there are Americans working, Social Security will have this steady, reliable source of income. It would take an Act of Congress to end this source of revenue. And if no Americans were working, our troubles would be a lot greater than Social Security’s financing!

Social Security is conservatively managed. Every year, its income and benefits are projected out not just five, 10, or 15 years, but 75 years. It is unsurprising that projections out that far into the future may sometimes show a deficit. And current projections do show a deficit, manageable in size and almost two decades away. That should be addressed, but it is nothing to be alarmed about, certainly nothing that calls for the loaded, misleading, emotionally charged cry of bankruptcy! The United States is the wealthiest nation in the world at its wealthiest moment in history. Not only can we afford the level of benefits called for in current law, we can afford increased levels of benefits and expanded kinds of benefits – and as we argue in our book, Social Security should be expanded.

The accompanying myth to the bankruptcy myth is that Social Security is a big contributor to the national debt. Why is this a flawed accusation?

By law, Social Security does not and cannot contribute to the national debt. By law, it can only pay benefits if it has sufficient revenue to cover every penny of the cost (including all administrative costs), and it has no borrowing authority. In fact, our Social Security system is a creditor of the United States. Whenever Social Security runs a surplus, it invests that surplus. Congress requires that those funds be invested in the safest investment on Earth – government bonds backed by the full faith and credit of the Unites States. The United States currently owes around $18 trillion to its creditors; $2.8 trillion of that $18 trillion is owed to Social Security. The bonds held by Social Security in trust for America’s working families have the same legal status as the bonds held by private pension plans, foreign governments and other institutions.

Another implied myth by opponents is that seniors are making out like bandits. Yet, the range of Social Security monthly checks is rather modest, to say the least, isn’t it?

Yes. Social Security’s benefits are modest by virtually any standard. They average around $15,000, about the same amount as full-time work at the minimum wage. They replace only about 40 percent of final pay of workers making average wages. And they are extremely low when compared to other countries’ public pension benefits. Social Security has been extremely effective in reducing poverty, but most seniors are either in poverty or just one economic shock away. Social Security’s modest benefits are vitally important, but no one is getting rich off of Social Security.

One of the more outrageous charges that the book responds to is that Social Security is a Ponzi scheme. Why is that such an inflammatory accusation?

A Ponzi scheme is a fraudulent, criminal activity, whose perpetrators intend to deceive their victims. Do those making the charge that Social Security is a Ponzi scheme really believe that President Franklin Roosevelt and every president since then, as well as all of our Congresses were coconspirators in an illegal activity? More to the point, Ponzi schemes are structures that are unsustainable, generally collapsing quickly. Those making the charge are seeking to undermine confidence in Social Security. But Social Security is this year celebrating the 80th anniversary of its enactment. It has stood the test of time. As I have explained above, its financing is solid and secure. There is no reason to doubt that Social Security will be with us as long as there is a United States, if that is what the American people want.

How do you respond to the attempt to make the funding of the program a generational conflict; i.e., that young people are increasingly buttressing the program, but there is little benefit for them now or in the future.

What most people don’t realize is that Social Security is the nation’s largest children’s program. It provides crucial support to children whose parents have died or become permanently disabled. It is the largest income source for grandparents supporting grandchildren who live with them. Social Security protects the entire family. It frees resources that would otherwise be spent by adult children on aging parents and allows those funds to be spent on those adult children’s children. And, of course, most children, we trust and hope, will one day grow old and count on Social Security just as today’s seniors do. Social Security is based on basic values we all share. One of those values is that, despite our differences, we are a united people.

Social Security is a program into which we all pay and out of which we all receive benefits in the event of death, disability or old age. This effort to turn one group of Americans, children and their supporters, against another group – seniors – is alien to the thinking of most Americans. We are parts of families. Families are not stronger if their older members are living in poverty. Families are not stronger if their younger members are uneducated or hungry.

Seeking to turn grandchildren against grandparents may be how Washington politicians and ivy-towered academics operate, but it is not how the rest of us do. One additional point: As we’ve discussed in an earlier question and answer, Social Security’s benefits are modest. Other countries with more generous benefits also tend to spend more on children. As the wealthiest nation in the world at the wealthiest moment in our history, we can afford to expand Social Security and spend more on our children, as well.

How do you respond to the proposal to raise the retirement age for receiving Social Security checks? Can you in the answer also explain the current tiered structure that increases yearly payouts to recipients based on when they first choose to begin receiving Social Security?

Let me state clearly, and then explain, an important point: Raising Social Security’s retirement age is an across-the-board benefit cut, whether you retire at age 62, age 66, age 70, or any age in between. Once the age is raised, you receive less per month, no matter at what age you retire, than you would have received prior to the age change. As we have already discussed, Social Security’s benefits are already low. They should be expanded, not cut.

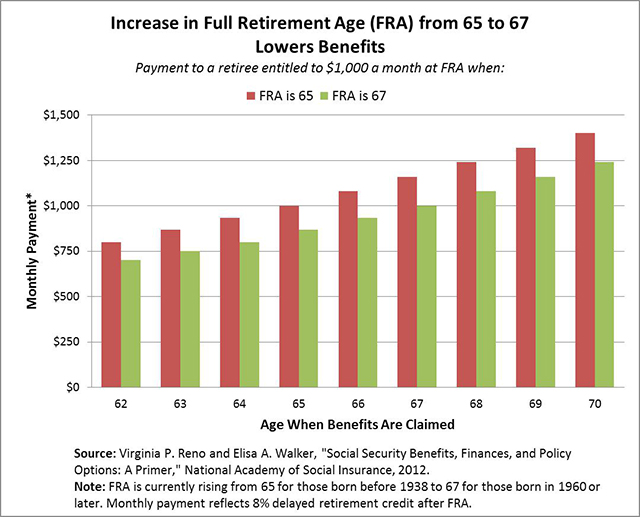

Under current law, Social Security’s statutory retirement age is already increasing from 65 to 67. (The chart below labels the retirement age stated in the Social Security Act as the “full” retirement age, but that label tends to confuse, I believe, so I am simply referring to the age that is gradually being increased from 65 to 67 as the “statutory” retirement age.) Though hard to understand without being thoroughly familiar with the way Social Security benefits are calculated, raising Social Security’s statutory retirement age is, as I just said, indistinguishable from an across-the-board benefit cut in retirement benefits. For every year that the statutory retirement age is increased, all retiree benefits are reduced by around 6 percent. As the following chart shows (reprinted from chapter 10 of our book, Social Security Works!), when the statutory or “full” retirement age is increased by two years, as is now gradually phasing in, workers receive lower benefits if they retire at age 62, 65, 67, 70, or any age in between.

The easiest way to understand it is to think of Social Security not as having a single retirement age, but rather a band of ages. Workers can choose to retire and begin to accept benefits at age 62. Benefits are increased for every month after age 62 that workers wait to begin to receive benefits, The idea is that the worker is receiving the benefits for one month less, so those benefits are increased slightly to make up for the lost month. The goal is to be neutral with respect to the decision when to retire. When the statutory retirement age is increased, benefits at every point on that band of ages are reduced.

The case for raising the retirement age is often defended by the facile sound bite that everyone is living longer. In addition to the point that raising the retirement age is nothing other than a benefit cut, the premise of the assertion is wrong. Not everyone is living longer, on average. Women in the lower half of the economic distribution have actually seen their average life expectancies decline in the last quarter century. Moreover, many workers in physically demanding jobs just aren’t healthy enough to work longer, regardless of what is happening to their overall life expectancies. The facile response is: Just because Wall Street CEOs are living longer, is that a reason to cut benefits across the board? The more serious response is that Social Security benefits are too low. We shouldn’t be cutting them; we should be expanding them.

Can you briefly discuss the war on the Social Security disability fund. What is the myth propagated – and currently active as legislation in Congress – that to transfer Social Security revenue into the disability fund is robbing Peter to pay Paul?

The current debate over Social Security disability insurance is simply the latest battle in an ongoing war against Social Security, which I describe in great detail in my first book, The Battle for Social Security (John Wiley & Sons, 2005). Because Social Security is so overwhelmingly popular with virtually all segments of the American people, opponents have taken to claiming that it is unsustainable, sought a way to force action, and championed undemocratic, behind-closed-doors negotiations to hammer out changes. So, as we detail in our book, Social Security Works!, the last six years or so have seen opponents argue that Social Security must be cut as part of a budget deal. The need to pass legislation raising the federal debt limit has been held hostage to efforts to reach such a bargain, though none were successful, and now the federal deficit is falling rapidly.

Consequently, the opponents have latched onto another must-pass piece of legislation. For no real reason, funding for Social Security’s benefit package are held in two different trust funds, the disability trust fund and the old age and survivors trust fund. Monies that are withheld from workers’ pay checks and matched by employers are simply divided by the government into the two funds. The problem is that Treasury and the Social Security Administration do not have the authority to direct what percentage of those contributions goes to each fund; that is specified by Congress, and so can only be modified by an act of law.

Now, just as investment portfolios have to be rebalanced from time to time, the amounts going to the two funds do as well. Indeed, the percentages going to the funds have been changed legislatively 11 times in the past, sometimes increasing the percentage going to one fund, sometimes reducing the percentage. We are now at the point where that rebalancing must occur again. If it were not done by the end of 2016, disability benefits could not be paid in full, because, as I explained before, benefits cannot be paid unless there is sufficient revenue to cover the costs. If a simple reallocation is made, both funds are projected to be able to pay full benefits through 2032. The problem is that opponents of Social Security are holding that legislation hostage to some unspecified “reform.”

On the very first day of the new Congress, House Republicans adopted rules, usually a pretty sleepy event. This time they included a rule which calls Social Security disability insurance a “broken program” (odd language for a rule), and which prohibits the simple rebalancing. Those of us who have been engaged in Social Security policymaking for a long time – I have been working on it for 40 years – know what is coming. A despicable strategy, intended to divide and frighten Americans. Claim that rebalancing is stealing from seniors to provide for workers who apparently are fraudulently pretending to be disabled. Then, seek to work out a negotiated agreement behind closed doors, where the American people won’t know whom to blame.

In the last battle – the one claiming Social Security is causing the deficit – seniors were the villains, supposedly “Greedy Geezers” robbing from children. This time, seniors are the victims of the disabled, the apparent Peter being robbed to help Paul.

Those who want to reduce or eliminate the Social Security Program contend that it is rife with fraud. Why is this an inaccurate claim?

Social Security is an incredibly efficient program. It spends less than a penny of every dollar on administration. Its test for who is disabled is perhaps the strictest in the world. Nevertheless, no insurance program, public or private, is without any fraud whatsoever. if dishonest people can collude with dishonest doctors, they can seek to build a case that they are disabled under Social Security’s strict standard.

According to those who have looked at the data, very few fraudulent cases – well less than 1 percent – slip by. Nevertheless, it is important for the Social Security Administration to work to reduce fraud even more, while being careful not to deny benefits to those who are truly disabled and have earned this protection. The cases of fraud have generally been discovered by Social Security Administration employees, but their numbers have been drastically reduced as a result of misguided cutbacks by Congress. The way to reduce even the relatively few cases of fraud is appropriately staffing the Social Security Administration. On top of that, the Social Security Administration has a hot line – (866) 269-0271 – where members of the public are invited to report suspected fraud. What should not happen though, is cutting the benefits of those who lawfully have earned them. Indeed, Social Security benefits should be expanded.

I’d like to move away from the myths about Social Security for the final question. Your book – written with coauthor Eric R. Kingson – makes the case for expanding the benefits to recipients of Social Security. Let’s consider the opposite possibility. What would be the impact on the United States today if Social Security were somehow – and let’s just be hypothetical here – eliminated?

The impact would be devastating not only for America’s working families but for the nation as a whole. Social Security has literally transformed the nation. At the time Social Security was enacted, every state but New Mexico had poor houses, primarily housing older people who had been wage earners their whole lives but had lost employment, couldn’t find new work, and had no family who was willing or able to take them in.

Children were often placed in orphanages, not because they had lost both parents, but because one had died and the other, usually the mother, couldn’t support them herself. At the time Social Security was enacted, growing old was something to be feared. At that time, it has been estimated that about half of all people over 65 had income below the subsistence level. The Center for Budget and Policy Priorities has calculated that today’s seniors would have the same high rates of below-poverty income – about one in two seniors – without Social Security, which accounts for more than half of the income of around two-thirds of today’s seniors. Without Social Security, we undoubtedly would return to the world where aging parents routinely moved in with their children. Those without children or whose children couldn’t take them in would likely find themselves on welfare and, perhaps, homeless. Permanent and serious disabilities and premature death leaving behind small children would likely once again almost certainly lead to greater homelessness and begging for handouts.

Other byproducts would be more subtle. We have rising levels of income inequality. That would rapidly become worse without Social Security, as well. In contrast, as we discuss in Social Security Works! expanding our Social Security system is a solution to a number of pressing challenges facing our nation.

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. We have hours left to raise the $12,0000 still needed to ensure Truthout remains safe, strong, and free. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.