When the economist Alvin Hansen first proposed the concept of secular stagnation, he emphasized the role of slower population growth in depressing investment demand. (His warnings were made moot by the postwar baby boom.)

Modern discussions have returned to that emphasis: Japan’s shrinking working-age population appears to be an important source of the country’s problems, and the slowing population growth in Europe and the United States are important indicators that we may be entering a similar regime.

But whenever I raise these points, I get questions from people who ask why I don’t regard slowing population growth as a good thing.

After all, it means less pressure on resources, less environmental damage, and so on.

What’s important to realize is that slower population growth indeed could, and should, be a good thing – but that what passes for sound economic policy is all too likely to turn this potentially good development into a major problem. Why? Because under the current rules of the game, there’s a strong “bicycle” aspect to our economies: unless they’re moving forward sufficiently rapidly, they tend to fall over.

It’s a pretty straightforward argument. To have more or less full employment, an economy needs sufficient spending to make use of its potential. But one important component of spending, investment, is subject to the accelerator effect: the demand for new capital depends on the economy’s rate of growth, rather than the current level of output. So if growth slows due to a falloff in population growth, investment demand falls – potentially pushing the economy into a semi-permanent slump.

Now, one could say that this should be easy to deal with; just reduce the interest rate sufficiently to sustain investment demand despite population slowdown. The problem is that the required real interest rate on safe assets may end up being negative, and is therefore achievable only if there is sufficient inflation – which runs into an ideological commitment to price stability.

This is basically a technical problem, and in a better world we would simply deal with that problem while enjoying the benefits of a less crowded planet. In this world, however, technical problems can in fact cause immense damage, because so few people are willing to think clearly about their nature. And that’s why we worry about slowing population growth.

Those French Job Creators

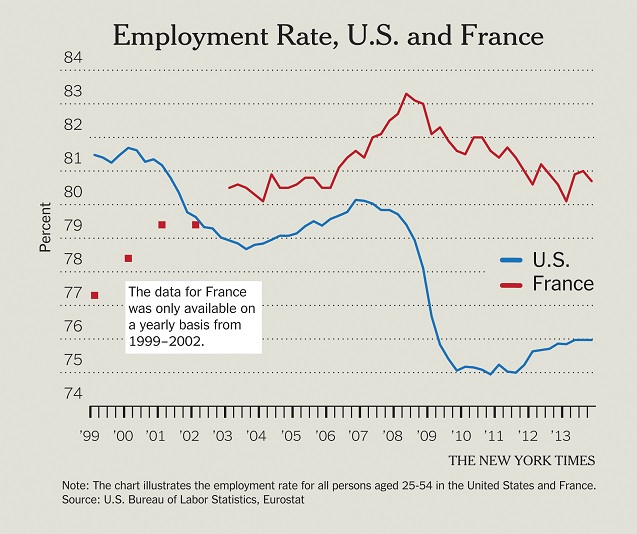

People are pretty down on European economic performance these days, with good reason. But mainly what we’re seeing is bad macroeconomic policy that is the result of premature monetary union plus austerity mania. That’s a very different story from the old version of Eurotrashing, which focused on Eurosclerosis – a persistent low employment rate allegedly caused by excessive welfare states.

Now, people like the economists John Schmitt and Dean Baker pointed out a long time ago that this story was out of date. If you looked at Europe in general, and France in particular, you saw that yes, people retired earlier than they did in the United States, and also that fewer young people worked – in part because they didn’t have to work their way through college. But on the eve of the economic crisis, employment rates among prime-working-age adults had converged.

Well, I hadn’t looked at this data for a while; and where we are now is quite stunning. See the chart.

Since the late 1990s we have completely traded places: prime-age adults in France are now much more likely than their American counterparts to have jobs.

It is strange how, amid the incessant bad-mouthing of French economic performance, this fact never gets mentioned.

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. To ensure Truthout remains safe, strong, and free, we need to raise $33,000 in the next 2 days. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.