There is considerable discussion about how people on the left should invest their money. For those who are socially conscious or who are anti-capitalists, this is usually an inherently distasteful endeavor. Stock markets are a central institution and symbol of capitalism after all, and they would not exist in the moneyless and classless society that many want to build.

It’s not surprising that so-called “socially responsible investing” (SRI) would seem attractive. In “socially responsible” mutual funds (bundles of stocks or bonds), fund managers screen companies based on their labor, environmental and social practices, depending on the fund. The result is an investment that is supposed to be socially responsible, while still generating a healthy return for its investors.

The Ideological and Practical Problems With “Socially Responsible” Capitalism

SRI funds have many problems. The overarching one is that these funds work within existing paradigms and do nothing to solve the crisis at the root of most of our problems: capitalism itself. In fact, “capitalism with a conscience,” together with business-friendly conceptions of sustainability or labor rights, can give cover to new and more insidious forms of exploitation. Many companies will produce slick corporate responsibility reports or conduct pro forma and staged audits of their suppliers, or simply focus their efforts on convenient nonsolutions. After coming under scrutiny over the treatment of those working for its global suppliers, Apple used the Fair Labor Association — a “public relations mouthpiece” — to conduct audits of its suppliers’ facilities. The results were unsurprising: The Economic Policy Institute concluded that “improvements in working conditions … have in most cases been modest, fleeting, or purely symbolic, while some key reform pledges have been broken outright.”

“Capitalism with a conscience” can give cover to new and more insidious forms of exploitation.

While audits like Apple’s might generate good publicity, they do little to ensure the company is being socially responsible. At the end of the day, profits are still what matter most, and this motive is at odds with fundamentally changing business practices.

The other issue is that the mutual fund industry, like many other parts of our financial system, has become more predatory in the last few decades. At the same time, many people have been forced to integrate more of their lives into the financial system. Because of that, the shift to retirement vehicles like 401(k) plans and to investment advisers who do not have a fiduciary duty to their clients means that the average investor faces many more pitfalls than before. Unlike Social Security and defined benefit pension plans, which provide consistent and predictable benefits and have few drawbacks, 401(k)-type vehicles are a boon to Wall Street and fund managers. As middlemen, workers in the financial industry take out a large chunk of money for themselves via management and fund fees (collectively called the fund’s expense ratio).

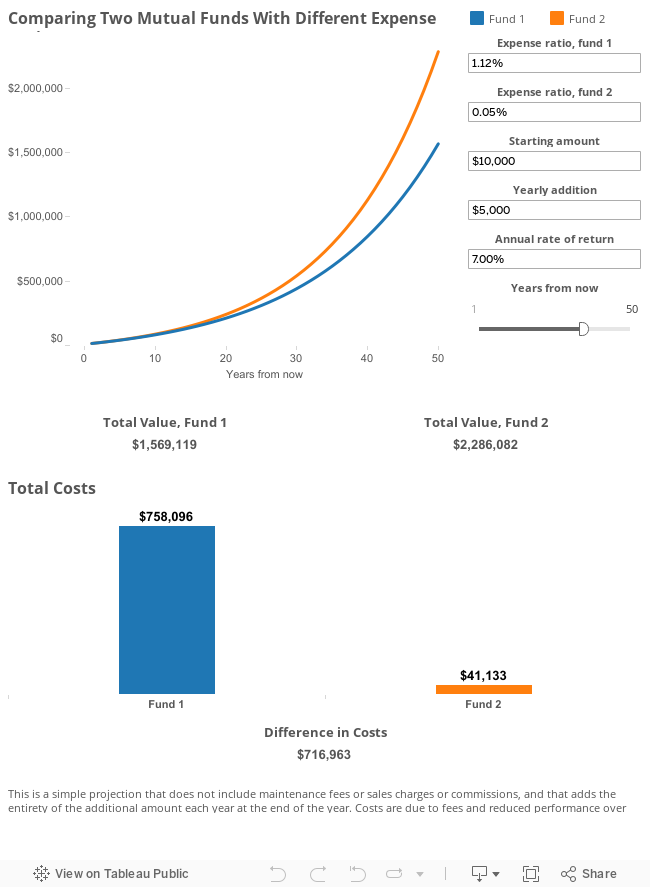

SRI funds are a good example of this exploitation. The expense ratios of these funds are generally much higher than normal mutual funds, and especially of index funds, which are not actively managed but rather track the market. The SRI funds monitored by the Forum for Sustainable and Responsible Investment, a trade group, average an expense ratio of 1.12 percent — the majority lining the pockets of the fund managers. In contrast, the expense ratio of index funds is often below 0.5 percent, and in the case of some funds, can be as low as 0.05 percent.

Lower expenses, over time, can produce significantly higher returns. Take, for example, a typical scenario saving for retirement (see interactive tool below):

Say a person invests $10,000 in fund with an expense ratio of 0.05 percent and adds $5,000 every year. They expect an annual return of about 7.00 percent on average, which is around the rate at which the stock market typically increases.

This will yield $2,286,082 in 50 years, costing about $41,133 in fees and reduced returns. The same investment in a fund with a 1.12 percent expense ratio will be worth only $1,569,119 after 50 years, and cost a staggering $758,096.

In addition to the ideological downsides of SRI funds, the practical downside is that they are very expensive.

So What Investments Make Sense?

The answer is surprisingly straightforward. If a person isn’t wealthy and needs to participate in the financial markets in order to hedge inflation or ensure financial security, investing in low-fee index mutual funds or annuities that cover broad segments of the market makes the most sense. Because index funds track the market, this money does not support anything in particular. It’s also an easy investment strategy, which is beneficial for people who don’t have the time or expertise to invest in other ways.

Practically, this is the best way to ensure a good return over time as well. Index funds, as opposed to actively managed funds (which pick and choose certain securities), have a history of good performance, and as previously mentioned, have much lower fees. For example, the average previous year’s returns of the funds listed by the Forum for Sustainable and Responsible Investment was -1.98 percent (only 61 out of 195 funds had a positive return); the average five-year return was 5.14 percent. In contrast, Vanguard’s Total Stock Market Index Fund, which aims to track the entire stock market, had a previous year’s return of 0.55 percent and a five-year return of 10.48 percent. High returns and low fees are essential to saving for retirement.

For most people, index funds are as close as they can get to opting-out of the financial system without jeopardizing future security.

While this is not unproblematic, for most people, index funds are as close as they can get to opting-out of the financial system without jeopardizing future security. A recent Truthout article took Vanguard, the firm that popularized low-fee index funds, to task for its investments in weapons manufacturers and prisons, among other things. While the article was thoughtful, the authors did not distinguish adequately between mutual funds, SRI funds and index funds in arguing that because Vanguard has large investments in malignant companies and questionable SRI funds, it is not a good place to invest money.

While no one should be under any illusions that Vanguard operates for the public good, Vanguard does drive the mutual fund industry toward less exploitative practices and lower fees. As the largest mutual fund company and a big proponent of index funds, it should also be unsurprising that it holds significant investments in every large company on behalf of its millions of investors. While the firm undoubtedly makes choices with regard to its actively managed funds, its index funds are separate from these decisions.

For a socially conscious person, I believe that it makes more sense to passively invest in the entire stock market rather than to try to play a whack-a-mole game and choose “good” companies and funds, which is a subjective assessment that is challenging to make. (Playing this game will also lead to considerable losses and fees, too, which many people cannot afford.)

For those who are wealthy or who are confident in their future economic security, the above considerations apply as well. But they should consider the extent to which they need to participate in financial markets at all. Instead of investing all of their money in index funds, they have much more leeway to back political convictions. This could mean investing in, or donating money to, individuals and organizations that they trust.

Toward the Future

No matter your financial situation, there are ways of advocating for a better financial system. For example, Social Security is an essential retirement program that is responsible for drastically reducing senior poverty and it can be an alternative to the exploitative financial system. It provides income that does not fluctuate based on the stock market, and has no middlemen. Because private savings and pensions no longer provide as much support in retirement as they used to — many people do not have pensions or the means or opportunity to save a significant amount of money via a 401(k) — Social Security is more important than ever.

Despite being exceedingly efficient and sustainable well into the future, Social Security is often unfairly attacked by those with political and ideological objections to its existence. But a burgeoning movement to expand the program is gaining traction and deserves support. This movement has turned the debate on its head: from a general acceptance that the program need drastic cuts to a consensus from the center-left that it should be expanded. (President Obama, after seven years in office, came out for expanding Social Security recently.)

Although financial markets aren’t very useful for supporting capitalism’s version of “social responsibility,” boycotts that that target companies are useful.

And although financial markets aren’t very useful for supporting capitalism’s version of “social responsibility,” boycotts that that target companies that profit off of fossil fuels, prisons and the occupation of Palestine, for example, are useful. Putting pressure on large investors, like universities or pension funds, to divest from these companies is essential to generating momentum for these movements. The same tactics can be used to pressure investment management companies, like Vanguard, to lean on the companies they invest in to adopt more transparent polices.

Capitalism will continue to appear to temper itself through myriad things — socially responsible investing, social impact bonds, philanthrocapitalism and venture philanthropy, token retirement savings plans like President Obama’s myRA, apps that make investing in fee-riddled funds easier, personal finance as a solution to poverty, etc.

Those looking for meaningful change must move past those red herrings, operate within capitalist institutions in principled ways and function outside of them when possible — all while laying the foundation for the future. Change won’t be as easy as making a particular kind of investment in the stock market; of that we can be sure.

Join us in defending the truth before it’s too late

The future of independent journalism is uncertain, and the consequences of losing it are too grave to ignore. To ensure Truthout remains safe, strong, and free, we need to raise $43,000 in the next 6 days. Every dollar raised goes directly toward the costs of producing news you can trust.

Please give what you can — because by supporting us with a tax-deductible donation, you’re not just preserving a source of news, you’re helping to safeguard what’s left of our democracy.